According to the 2021 Ghana Statistical Service report, approximately 2.46 million people in Ghana have a disability, representing 8% of the total population. (GSS, 2021)

Persons with any form of Disability

"If only people can stop assuming for us! We can actually work, when we get the right assistance”.

Entrepreneur with disability, Accra

Majority PwD on the streets have at least basic level education. A few have up to Senior High level of education. Technical and tertiary education is considered higher that would put one in a gainful and decent employment.

Registration of Business Names Act, 1961(Act 151)

Business Names also known as a sole proprietorship (one-man business) registered by one (1) person who takes all business decisions and all liabilities are unlimited i.e. makes profits alone and bears losses alone.

Credits: Office of the Registrar of Companies

| Name | General Overview | Offices |

|---|---|---|

| The 1992 Constitution of the Republic of Ghana | Establishes the fundamental principles and framework for governance in Ghana. | National |

| Business Operating Laws | N/A | N/A |

| Ghana Companies Act, 2019 (Act 992) | Governs corporate structures and operations in Ghana. | All types of businesses |

| Income Tax Act, 2015 (Act 896) As Amended | Regulates corporate and personal income taxes, withholding taxes, gift tax, royalties, and industry-specific taxes. | All types of businesses |

| Value Added Tax Act, 2013 (Act 870) | Regulates value-added tax (VAT) for businesses. | All types of businesses |

| National Health Insurance Levy | A levy supporting Ghana's National Health Insurance Scheme. | All types of businesses |

| GetFund Levy | A levy contributing to the Ghana Education Trust Fund. | All types of businesses |

| Electronic Transfer Levy Act, 2022 (Act 1075) | Imposes a levy on electronic transfers. | All types of businesses |

| National Pensions Act, 2008 (Act 766) As Amended | Mandatory SSNIT (Social Security and National Insurance Trust) payment | All types of businesses and persons |

| Certifications | N/A | N/A |

| Business Operating Permit | A permit required for all types of businesses issued by the District, Municipal or Metropolitan Assemblies. Or relevant national body. | All types of businesses |

| Food and Drugs Authority Certification | Sector-specific certification related to the food and drugs industry. | Sector Specific |

| Ghana Standards Authority Certification | Sector-specific certification related to the … | Sector Specific |

| Social Welfare Certification | Required for non-governmental organizations. | Non-Governmental Organizations |

| Statutory Audit | Mandatory audit for all types of businesses. | All types of businesses |

| Industry or Sector Specific | N/A | Sector Specific |

| Employment Laws | N/A | N/A |

| Labour Act, 2003 (Act 651) | Regulations governing employer-employee relationships. | All types of businesses |

| National Employment Policy (NEP) 2015 | N/A | All types of businesses |

| Name | General Overview | Offices |

General Tax Incentives: Business Types

| Sector/Business | Period of Tax Holiday | Special Corporate Income Tax Rate (%) | Actual Tax Rate After Tax Holiday (%) |

|---|---|---|---|

| Agro processing business conducted wholly in the country | First Five (5) years | 1 | 25 |

| Cocoa-by product business wholly in the country | First Five (5) years | 1 | 25 |

| Tree crop farming | First Ten (10) years | 1 | 25 |

| Cash crops or livestock (excluding cattle) | First Five (5) years | 1 | 25 |

| Cattle farming | First Ten (10) years | 1 | 25 |

| Waste processing business | First Seven (7) years | 1 | 25 |

| Rural Banks | First Ten (10) years | 1 | 8 |

| Real Estate (certified low-cost housing) | First Five (5) years | 1 | 25 |

| Sector/Business | Period of Tax Holiday | Special Corporate Income Tax Rate (%) | Actual Tax Rate After Tax Holiday (%) |

Agro-Processing Sector

| Location of Plant | Corporate Income Tax Rate (%) |

|---|---|

| Accra | 20 |

| Tema | 20 |

| Other Regional Capitals (except Northern, Upper East and Upper West Regional Capitals) | 15 |

| Outside regional capitals | 10 |

| Northern, Upper East and Upper West Region (including their capitals) | 5 |

| Location of Plant | Corporate Income Tax Rate (%) |

| Location of Plant | Corporate Income Tax Rate (%) |

|---|---|

| All regional capitals except Accra and Tema | 1.875,00 |

| Outside regional capitals | 125,00 |

| Location of Plant | Corporate Income Tax Rate (%) |

Product Specific Incentive

Exporters of Agricultural Products

Companies which engage in the exportation of non-traditional products such as horticultural products, processed and raw agricultural products grown in Ghana other than cocoa beans, wood products other than logs and timber, handicrafts and locally manufactured goods enjoy a concessionary tax rate of 8%.

Deductions

An expense is deductible if it is wholly, exclusively and necessarily incurred by the person in the production of the business or investment income for the year.

A deduction shall be disallowed for an expense that is of a capital nature.

An expense that is of a capital nature includes an expense that secures a benefit that lasts for more than twelve (12) months.

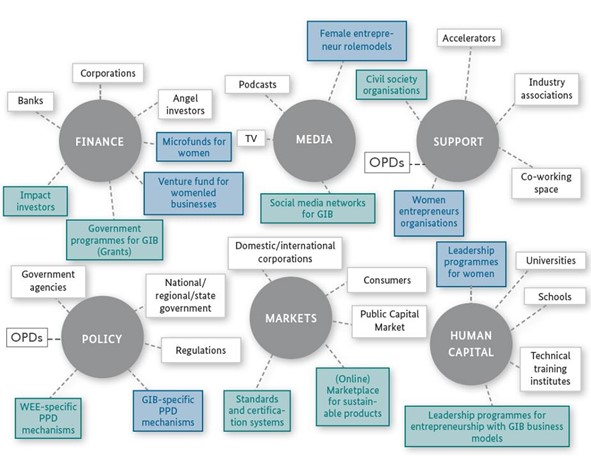

The entities providing assistance within the entrepreneurial ecosystem in Ghana, specifically focusing on the Greater Accra and Eastern regions, are diversified across various sectors, including Finance, Media, Support, Human Capital, Markets, and Policy. This distribution is illustrated in the diagram.

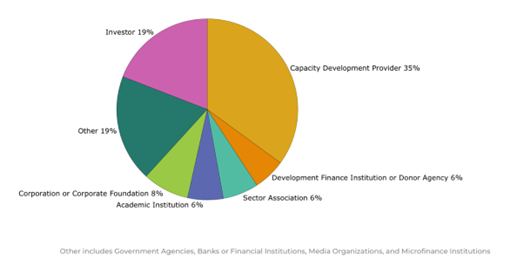

The analysis shows that the Ghanaian ESO ecosystem is supply driven, as ESO providers and SMEs are almost entirely dependent on the provision of subsidies by the government and donors.